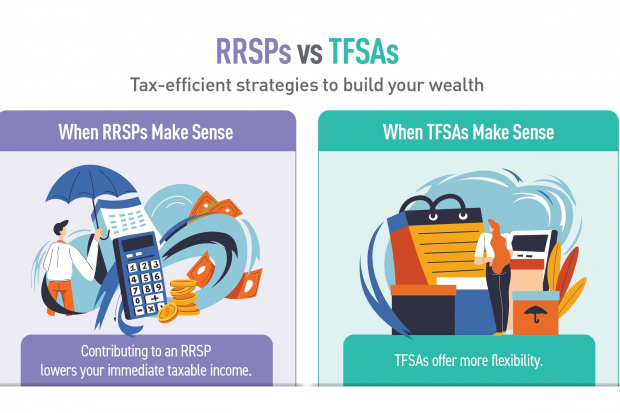

Two things in life are certain: taxes and something else. (Plugs ears). We all have to pay our fair share, but RRSPS and TFSAs allow you to be strategic about the timing and amount of taxes you’ll pay.

Of all the big-ticket items awaiting you in the land of Financial Responsibility, the idea of investing for the first time can feel like one of the most intimidating processes of all. But it doesn’t have to be that way.

There’s a saying about lawyers that doesn’t exactly bode well for retirement planning: “Most lawyers live well, work hard and die poor.” And there’s more of that middle part – the working part – for lawyers than for most.

If you’ve ever tried to sleep while a car alarm goes off outside your window, you know: if the alarm lasts long enough, you kind of get used to it. (Unless, of course, it’s your car). But just because you get used to stress doesn’t mean it isn’t there.

There are tax-efficient structures in place to give Canadians of all ages a bit of help – but too few of us are taking advantage of them. Here’s a list of differences between RRSPs and TFSAs to help you decide which one makes more sense for you.